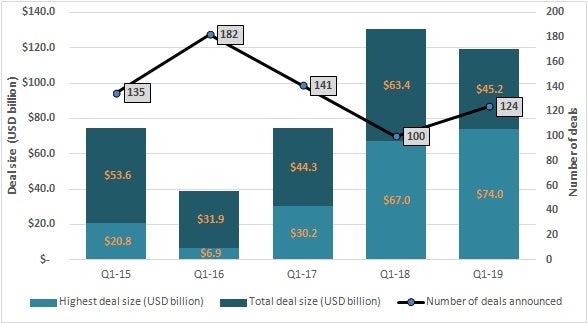

During the first quarter of 2019, Cortellis Deals Intelligence registered 124 new mergers and acquisitions (M&A), a 24% increase from 100, quarter on quarter vs. last year, as part of its ongoing coverage of M&A activity in the life sciences sector (see Figure 1). However, total disclosed deal value declined by 9% to $119.2 billion from $130.4 billion, although Bristol-Myers Squibb’s $74 billion approach for Celgene showed that mega-mergers continue to be a real force in the current climate.

Figure 1: M&A deal activity in Q1, 2015-2019: New M&A volume increased by 24% but total deal value declined by 9%. Source: Cortellis Deals Intelligence

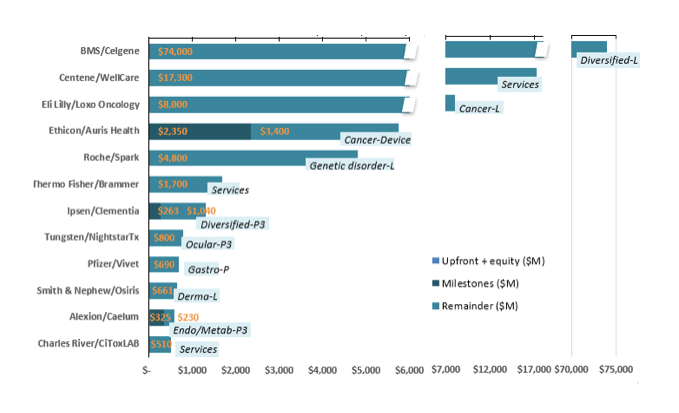

We tracked 24 new M&As worth in excess of $100 million with 12 of these worth more than $500 million each, contributing a total of $116.1 billion; this amounted to 97.4% of the total disclosed figure of $119.2 billion (see Figure 2). Pharmaceutical mega-mergers continued to dominate the quarter as the major players looked to combine pipelines, particularly in the gene-specific oncology and ocular space, enhance R&D, distribution and commercialization capabilities and improve market share.

Figure 2. Top M&As in Q1, 2019 disclosed by deal size (L – launched; P-3 – Phase III; P – preclinical): 12 high-value M&As worth in excess of $500 million were tracked. Source: Cortellis Deals Intelligence

Big deals: BMS-Celgene, Lilly-Loxo, Roche-Spark

Bristol-Myers Squibb (BMS) looked to strengthen its presence in the inflammatory and immuno-oncology space with its $74 billion approach for Celgene as it identified synergies across their pipelines. BMS looks to have set its sights on lenalidomide (Revlimid), an oral tumor-necrosis factor-alpha inhibiting thalidomide derivative widely available for myelodysplastic syndrome with 5q deletion chromosomal abnormalities and multiple myeloma, which generated $9.6 billion in sales in 2018 and is set to hit $13.3 billion in 2021, according to Cortellis Competitive Intelligence.

While BMS’s active drugs portfolio, analyzed by indication, heavily weighs towards pre-registered and launched assets and Celgene’s consists mainly of early stage programs, synergies exist in the areas of oncology, immunity and inflammation. Discussions remain ongoing.

Eli Lilly expanded in the oncology area capturing Loxo Oncology for $8 billion. Loxo was established in 2013, focusing on developing genomic alteration-driven, patient-specific anticancer treatments using companion diagnostics and immunohistochemistry testing. Loxo’s lead asset is larotrectinib sulfate (Vitrakvi), a tropomyosin receptor kinase inhibitor recently available in the U.S. for solid tumor. Its RET inhibitor, LOXO-292 (selpercatinib), has shown good clinical progression in phase I/II. At the same time, Bayer exercised an option for exclusive U.S. commercialization rights as part of a $1.6 billion license with Loxo stemming back to November 2017.

Roche took steps to pursue market growth in genetic diseases by targeting Spark Therapeutics for $4.8 billion. The Children’s Hospital of Philadelphia spin-out is built around its adeno-associated viral (AAV) gene therapy platform, generating a portfolio focused on orphan genetic complications, such as inherited retinal, liver and neurodegenerative diseases, via a regulatory designation pathway. Its only launched product, voretigene neparvovec (Luxturna), an intraocularly injected AAV that delivers the RPE65 gene to treat retinal pigment epithelium, which is licensed to Novartis, is forecast to obtain billion-dollar revenue status in 2024, according to Cortellis Competitive Intelligence.

Q1 M&A activity was low across Asia-Pacific

M&A activity across companies based in key Asia-Pacific regions was low this quarter. Japan led the way with a disclosed $86.1 million, compared to China with $36.6 million. Deal volume was also down with figures in the low single digits, led by Japan with three M&A type deals announced.

Interestingly, the few M&As announced by APAC-based companies focused on manufacturing capabilities, with firms in both China and Japan targeting organizations with established antibody manufacturing technologies and facilities.

Editor’s Note: All data contributing to this analysis was sourced from Cortellis Deals Intelligence, from Clarivate Analytics.

To see the Cortellis team’s full Q1 M&A report, including in-depth tables on the BMS-Celgene, Lilly-Loxo and Roche-Spark deals, as well as more analysis on Asia-Pacific activity and preview of Q2, click here.