A persistent and complex challenge

Drug shortages are a persistent and increasingly complex challenge. In the United States alone, the FDA reported national shortages of 258 unique active ingredients between 2018 and 2023. Far from being a simple inventory issue, these shortages represent not only a threat to patient care and a significant source of strain on the healthcare system but also a direct risk to pharma revenues and market stability.

Although regulatory bodies like the FDA actively monitor and respond to hundreds of shortages annually, the root causes often lie deep within the intricate, globalized pharmaceutical supply chain.

Hidden points of failure

In a system consisting of interconnected dependencies, global factors can have a profound local impact. The ongoing closure of the Strait of Hormuz serves as a real-world example of how a geopolitical event can threaten the global supply chain, with concerns about delayed shipments of everything from the petroleum needed to produce packaging to active pharmaceutical ingredients (APIs) and finished drugs.

These disruptions highlight how points of failure can emerge anywhere in the ecosystem, from the sourcing of APIs and other raw materials to issues with drug delivery devices, manufacturing facilities, storage, distribution and even the underlying data infrastructure. The risks compound when visibility into these complex networks is limited and sourcing options are few.

Building resilience through data-driven intelligence

To proactively minimize risk, more resilient supply chains are needed. The ability to effectively identify alternative suppliers, monitor the impact of geopolitical and environmental risks and understand the entire upstream supply network is key to ensuring the consistent and reliable delivery of therapies globally.

Oncology drugs exemplify how shortages can lead to poorer clinical outcomes due to delayed treatment initiation, interruptions in treatment continuation and use of less effective or less safe therapies. A recent study found that, of the 15 oncology drugs impacted by shortages between 2023 and 2025, 12 had shortages lasting >2 years.

The authors categorized the reasons for shortages across the 15 drugs into nine themes:

- Manufacturing quality issues, such as plant shutdowns, Good Manufacturing Practice (GMP) or sterility violations, capacity limits and contamination events

- Limited source dependency, including reliance on one or a few manufacturers (API or finished dose) and minimal redundancy

- Regulatory bottlenecks, such as import bans, delayed approvals or forced extensions for allocation/expiration

- Global over-reliance on overseas supply chains or off-shored production

- Absence of buffer stocks, often resulting from the use of just-in-time inventory, which means small disruptions have a bigger impact

- Demand surges driven by label expansions, guideline changes or shortage-driven substitutions

- Low economic incentives that discourage investment in backup capacity

- Shortages of API or other raw materials

- Shelf-life constraints or complex logistics that preclude stockpiling (e.g., radiopharmaceuticals)

To understand the supply chain and its vulnerabilities for each drug, the authors had to consult multiple sources, including the FDA Drug Shortages Database, FDA Orange Book and DynaMedex drug database as well as FDA warning letters, recalls and enforcement actions.

For pharma companies needing to identify the potential vulnerabilities in their supply chains and develop appropriate risk management plans, this type of investigation takes considerable time and resources. A single source of integrated intelligence, such as Cortellis Product Intelligence, streamlines this process.

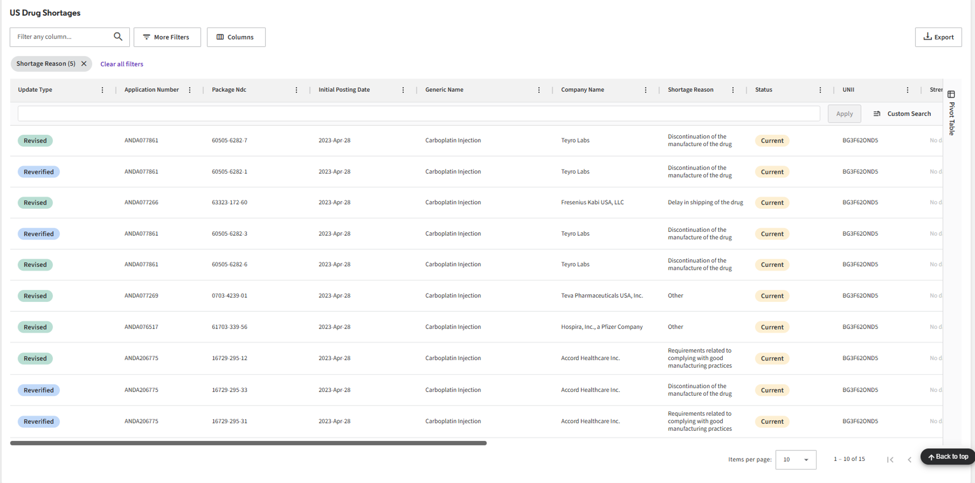

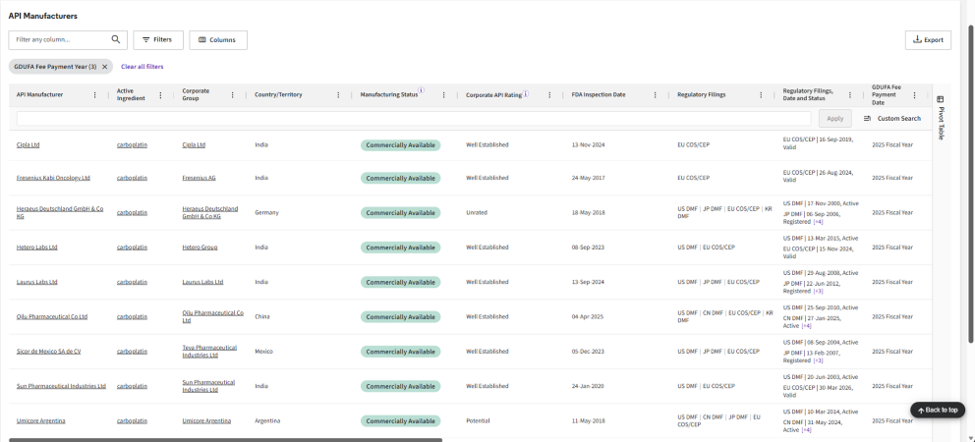

Carboplatin, a commonly used chemotherapy across multiple oncology indications, can be used as an example of how Cortellis Product Intelligence can enhance visibility into supply risks. Carboplatin has experienced shortages in the U.S. since 2023 for a number of reasons including discontinuation by multiple manufacturers, GMP compliance issues, increased demand and delayed shipping, as shown in the Cortellis Product Intelligence US Drug Shortages tab.

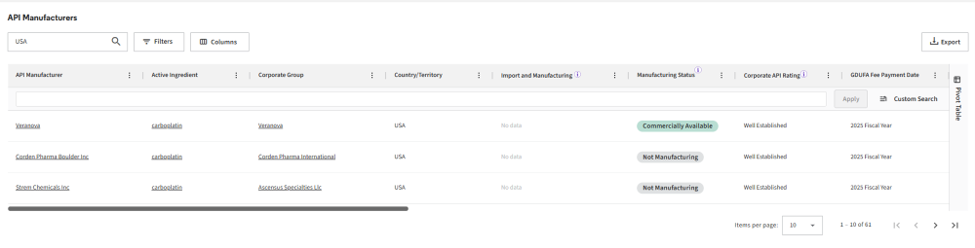

According to Cortellis Product Intelligence, only one API manufacturer is active in the United States, meaning that the API needs to be sourced from overseas locations, introducing potential geographic vulnerabilities.

Well-established API manufacturing companies are primarily located in India, with a few in other locations.

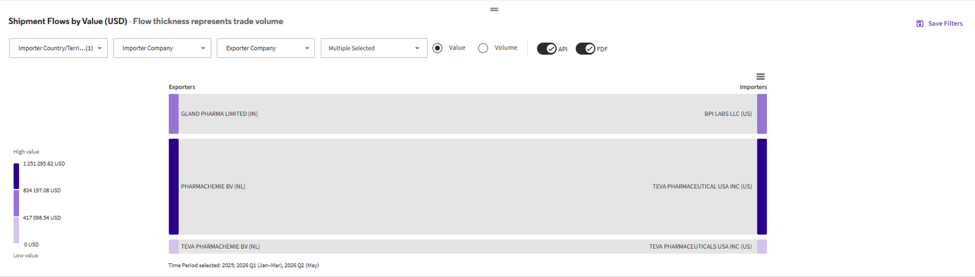

The primary importer of carboplatin into the United States is Teva Pharmaceutical USA from its own subsidiaries, Pharmachemie BV and Teva Pharmaceutical BV, both located in the Netherlands.

In addition, this landscape is characterized by multiple pharma companies vying for the same supply from this limited set of overseas API manufacturers as well as the short list of U.S.-based importers.

With this information, pharma companies can understand where the greatest risks (ie, whether that’s a dependence on one geographic location for API manufacturing, the need to ship API and finished goods around the world to reach the U.S., or the path into the U.S. through a dominant importer — or all of the above). Strategic decisions can be made to address the greatest source of risk to ensure a consistent, reliable supply of critical drugs like carboplatin. Actions could include diverse partnerships, investments in capabilities across multiple manufacturers or potential onshoring.

Ultimately, in an era of increasing global interdependence, the ability to anticipate and mitigate these multifaceted risks is paramount to building a truly resilient supply chain.

We will be sharing our latest analysis on the global API manufacturing landscape in a presentation at CPHI Milan on October 6.

Contact our team to schedule a demo and learn more about how you can stay ahead of the next disruption with Cortellis Product Intelligence.

Related insights

The latest news, technologies, and resources from our team.