本記事は英文ブログを日本語に翻訳再編集(一部追記を含む)したものです。本記事の正式言語は英語であり、その内容・解釈については英語が優先します。

AMARDEEP SINGH

Principal Analyst, Clarivate

最近のNRDLの更新により、中国本土では革新的な治療法に対する市場アクセスと償還の環境が改善していることが明らかになりました。しかし、これはNRDLへの登録と引き換えに、メーカーが提示しなければならない大幅な価格引き下げという代償を伴うものです。このような値下げは、中国本土での市場アクセスを獲得する価値があるのでしょうか?また、最近のNRDLの更新から、他にどのような傾向が見られ、製薬会社はこれらの傾向に適応するために何ができるのでしょうか?クラリベイトのエキスパートAmardeep SinghとAkash Sainiが以下の記事で解説しています。

成長を続ける中国本土のヘルスケア市場では、新しい治療法に対するアクセスと保険償還の環境を整えることが、常にアンメットニーズとなっています。病院で購入する医薬品のアクセスと保険償還を改善する目的で2000年に設立された同国の国家医療保険償還医薬品リスト(NRDL)は、2017年までに3回しか更新されず、主にジェネリック医薬品の償還に重点が置かれていました1。しかし、2017年以降、毎年定期的に更新され、プレミアム価格の革新的な治療法が多くNRDLに含まれていることから、このアンメットニーズがようやく満たされつつあることが示唆されています1。クラリベイトのChina In-Depthによると、NRDL交渉中に発生した償還や大幅な価格引き下げのおかげで、リストに追加された多くの革新的な治療薬が、欧米市場と同等の患者の取り込みを開始していることが示唆されています。

2020年12月に行われた最新のNRDL更新では、過去10年間で最大の119品目の医薬品がリストに掲載され、そのうち50品目が欧米の医薬品でした。過去4年間に見られた2桁の平均値引き(2015年58%、2017年44%、2018年58%、2019年61%)と同様に、今回の更新でも平均51%という途方もない値下げが施行されました。国家医療保障局(NHSA)は、これにより20211年に中国の患者の医療費が約43億米ドル削減されると考えています。各省の保険償還医薬品リスト(PRDL)が地方レベルの調整を行うことを事実上禁止されているため、省レベルでの償還はもはや現実的な選択肢ではなく2、医薬品メーカーにとってNRDLへの登録はさらに重要な意味を持つようになりました。

中国本土で事業を展開する医薬品メーカーにとって、NRDLの更新が定期的に行われるようになり、ますます欠かせないものとなっています。本記事では、過去4回のNRDLの更新から浮かび上がってきた3つの重要な傾向を分析し、中国での市場アクセスおよび償還戦略を設定するメーカーへの提言を行います。

最近のNRDL更新に見られる3つの傾向

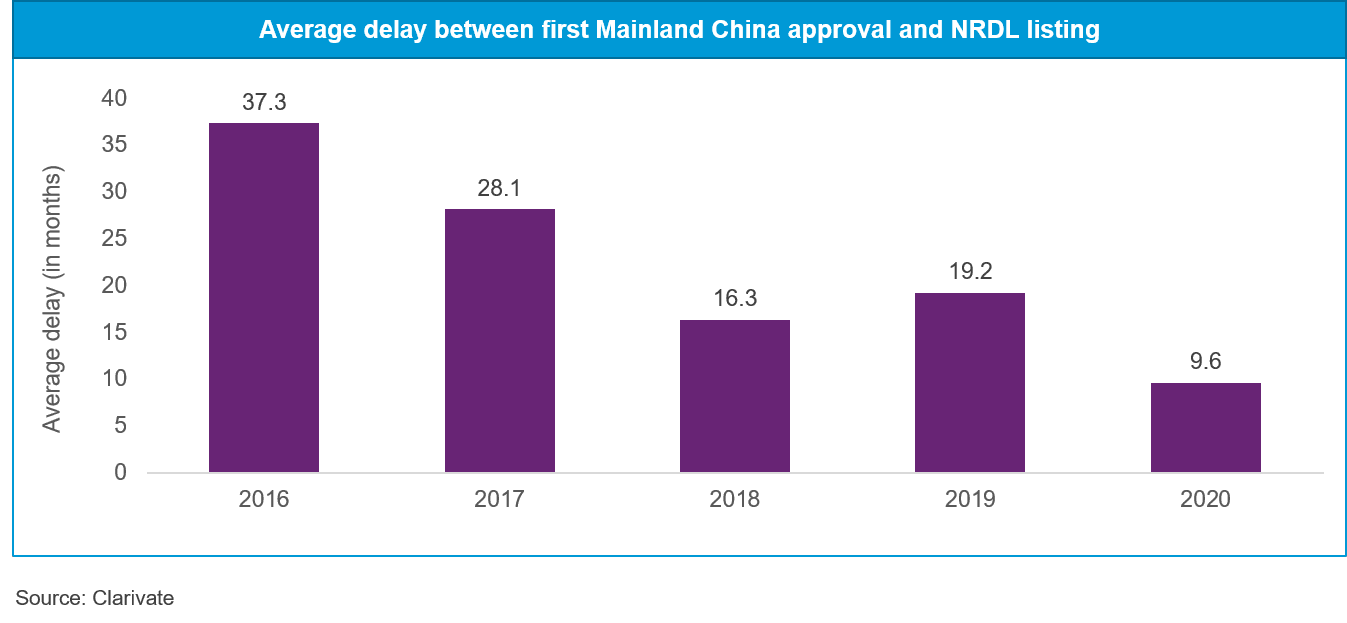

承認されてからNRDLに掲載されるまでのタイムラグの減少

クラリベイトの China In-Depthによると、中国本土で最初に承認されてからNRDL掲載までの平均的なタイムラグは、2016年の37カ月から2020年にはわずか10カ月と劇的に短縮されています。2020年初頭に承認されたいくつかの主要な抗がん剤は、同年のNRDL更新に間に合いましたが、これはかつてないことでした。

NRDLへの登録の遅れを減らすことで、製薬メーカーは特許保護を失う前に市場への浸透を最大化することができ、他のイノベーターを奨励し、新しい治療法を開発したメーカーに報いることができます。

NRDL登録後、ブランド治療薬の売上が大幅に増加

クラリベイトのChina In-Depthによると、ほとんどのブランド治療薬は、NRDL搭載後、交渉で大幅な価格引き下げを受けたにもかかわらず、売上が急増しています。ロシュ社の報告によると、ハーセプチンとアバスチンは、2017年にNRDLに組み込まれた後の2年間で、それぞれ2倍、3倍以上の売上を記録していますが、いずれも60%以上の値下げを行っています3。

この傾向は、患者の負担が大きく、革新的な治療法に対する膨大なアンメットニーズがある、価格に敏感な市場である中国本土でのNRDLへの組み入れには、急な価格引き下げが必要であることを示唆しています。

NRDLに掲載される国内企業の認知度の向上

歴史的に見て、NRDLに含まれる国内メーカーは、ほとんどがジェネリック医薬品か漢方薬に限られていました。しかし、中国本土における国内イノベーションの推進により、多くの国内企業が登場し、革新的な医薬品市場において多国籍企業と競合するようになってきました。その結果、中国本土の医薬品市場における国内で開発された革新的な医薬品のシェアは近年著しく拡大しており、NRDLにおけるその足跡も更新のたびに拡大しています。

2019年と2020年のNRDL更新では、国内企業が新薬の総掲載数の35%と44%を占めています1。クラリベイトの専門家は、国内メーカーが価格面での妥協を惜しまないことで、NRDL交渉での勝利に有利な立場にあると考えており、したがって、NRDLにおける彼らの可視性は今後の更新でも増加し続ける可能性があります。中国本土のPD-1/PD-L1阻害剤市場は、おそらく世界で最も混雑していると思われますが、この考えを裏付けるように、国産のPD-1阻害剤4製品すべてがNRDLに登録された一方で、Merck社のキイトルーダとBMS社のオプジーボは依然として除外されています。

メーカーへの3つの提言

NRDLへの早期登録

早期のNRDL登録は、より早く、より高い市場浸透性を保証し、メーカーにとっては医薬品のより良いライフサイクル管理を可能にします。したがって、中国本土での承認申請に先立って、あるいはそれと並行して、NRDL交渉の準備を開始するメーカーは、新薬の商業的可能性をより十分に実現することができるでしょう。よく考えられた価格戦略は、交渉を成功させる可能性を高めます。

NHSA (National Healthcare Security Administration) では、NRDL掲載のための正式な申請書を募集しています。これは、交渉対象となる医薬品の選定が、メーカーの意見を聞かずに専門家の委員会によって行われていた従来の方法とは異なり、メーカーにとってより透明性の高いプロセスとなっています。規制当局の承認からNRDL掲載までのタイムラグが短縮され、NRDL交渉を申請できるようになったことで、このプロセスはこれまで以上に効率的で透明性の高いものとなり、早期に行動するメーカーはその恩恵を受けることができるでしょう。

NRDLへの登録をサポートするリアルワールドデータの使用

NMPAは、規制当局への申請を裏付けるリアルワールドデータをエビデンスとして認めるようになりました4。2020年6月、サノフィは、最近始まったHainan Bo’Ao Lecheng International Medical Tourism Pilot Zoneスキームを活用し、このパイロットゾーンでNMPAによる正式な規制当局の承認なしに医薬品の承認が可能となり5、アトピー性皮膚炎の治療薬であるデュピクセント (dupilumab) を発売しました。同社は、パイロットゾーンの中国人患者からデュピクセントの有効性に関するリアルワールドエビデンスを得て、NDA申請から6ヶ月以内の2020年6月にNMPAの承認を取得したと考えられます。また、デュピクセントはその後すぐに、2020年に更新されるNRDLにも登録されました1。

中国本土では、規制当局への申請にリアルワールドデータの使用が正式に認められているため、メーカーはNRDLへの登録申請をサポートするために、リアルワールドエビデンスを用いて、安全性や有効性だけでなく、費用対効果もアピールする機会があるかもしれません。

競争力を維持するための代替パスウェイへの注力

NRDLへの登録交渉に失敗した場合、医薬品メーカーは、患者支援プログラム(PAP)の提供、医療経済学的価値の優位性を示すための自主的な価格引き下げ、価格交渉の意思表示など、患者アクセスの代替ルートに焦点を当てることができます。これらの方法は、短期的には患者さんの自社製品へのアクセスを向上させるだけでなく、将来のNRDL更新時に交渉を成功させる可能性を高めることにもつながります。例えば、PD-1阻害剤「キイトルーダ」と「オプジーボ」の価格交渉に連続して失敗したMerck社とBMS社は、これらの医薬品を患者さんにとって大幅に値ごろ感のあるものにする魅力的なPAPを提示しました。

このような取り組みにより、メーカーは市場での存在感と医師からの信頼を高め、最終的にNRDL交渉で勝利することができます。さらに、メーカーは中国本土で成長している民間保険市場を活用し、民間保険会社と提携してそのプランに掲載される可能性もあります。

NRDLの今後

中国本土では、ここ数年、NRDLを定期的に更新し、革新的で高価な医薬品を含むようにNRDLの範囲を拡大することで、安価な医療の実現に向けて大きな前進を遂げました。しかし、NRDLが唯一の償還手段となったことで、メーカーは薬価交渉の際に毎年大幅な値下げが行われ、薬価収載に向けて大きな圧力を受けることになりました。このような価格引き下げは、長期的にはNRDLへの上場に有利に働く可能性がありますが、価格交渉に失敗したからといって、その医薬品が「終わり」を迎えたと考えるべきではありません。メーカーは、患者のアクセスを確保するための別の方法を模索することができます。例えば、患者支援プログラムを提供したり、限られた公立病院セクターの外に進出したり、成長する民間医療保険市場の獲得に注力したりすることができます。

この記事は、クラリベイトのアナリストがChina In-Depthのデータと分析をもとに作成したものです。China In-Depthには、患者数、アクセスと償還の環境、治療パラダイム、パイプライン、薬剤レベルの予測などが含まれます。

中国本土のヘルスケア市場と疾患別トレンドに関する情報へのアクセスについては、こちらをご覧ください。

References

- nhsa.gov.cn

- gov.cn/zhengce/2020-03/05/content_5487407.htm

- roche.com/investors/annualreport19.htm

- nmpa.gov.cn

- lecityhn.com/2020-07/01/c_505419.htm