The United States health insurance market is seeing some of the largest enrollment changes ever, resulting in significant disruption in medical and drug coverage for millions of Americans.

Medicaid and health insurance exchange enrollment is shifting dramatically across the U.S. following the end of the COVID-19 public health emergency, which lapsed in May 2023.

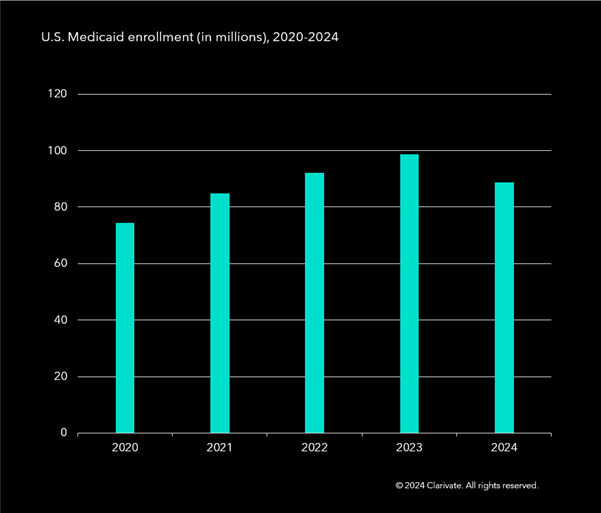

According to Clarivate’s latest enrollment data, as of January 2024, Medicaid enrollment had plummeted by nearly 9 million compared to six months prior. This drop was caused by the ending of the redetermination of eligibility process for Medicaid that was enacted under the government’s emergency declaration.

Medicaid enrollment fell with the end of COVID-19 emergency measures

Source: Clarivate enrollment data as of January for each year (January 2024 enrollment is projected)

The considerable enrollment loss in Medicaid has presented a growth opportunity for health exchange enrollment nationwide, with membership increasing by more than 4 million.

Clarivate’s new enrollment survey numbers, which are scheduled for release in June, shed light on the impact of Medicaid verification efforts in all 50 states and the District of Columbia. States have taken a wide variety of approaches to re-verifying eligibility.

Several states moved quickly to terminate enrolment of those that did not respond to mailed questionnaires, resulting in large numbers of families applying to be restored to coverage. News stories have reported these members saying they never received the state’s packet in the mail and only found out they had been cut off upon going to the pharmacy.

Medicaid’s managed care organizations have followed their states’ actions closely, using their own outreach to help their members reapply or find subsidized coverage through insurance exchanges established by the Affordable Care Act.

In its Q4 earnings call, Molina noted that roughly one-third of its members had been terminated early on, but that more than 70% were removed for “procedural” reasons, not because they were determined to be ineligible. “As a result, we are seeing nearly 30% of those termed being reconnected, and we expect these numbers to grow,” said Molina CEO Joseph Zubretsky. “Given the high number of procedural terminations and increasing state and CMS interventions, we expect reconnects will likely continue decreasing currently reported membership losses.”

Reconnection to coverage is also variable by state, with some states forcing families to re-apply for coverage, a process that can take weeks.

Insurance exchanges underwent their largest single-year enrollment growth since their inception in 2014, pushing exchange enrollment to yet another all-time high.

After staying relatively flat for several years, enrollment growth took off in 2021 after an expansion in federal subsidies for silver-level plans passed in the American Rescue Plan and was then renewed through 2025 in the Inflation Reduction Act. That supercharged exchange enrollment and made crossing from Medicaid to exchange coverage easier.

For 2024, 18% of enrollees were new to exchange coverage, according to the Centers for Medicare and Medicaid Services.

Several of the national for-profit insurers, including national exchange leader Centene and Elevance Health, mirror the trend, with exchange enrollment taking another big leap while Medicaid enrollment declined. Coverage for national carriers such as Elevance and UnitedHealth Group has extended to the group commercial market as well, an indication that Medicaid redeterminations have moved some losing Medicaid coverage back under group coverage.

The enhanced subsidies are a key factor in uninsured rates not spiking after so many Americans have lost Medicaid coverage. Astute insurers also worked to move people losing that coverage to exchange plans, where subsidies can defray most of the premium cost.

Many insurers use similar networks for Medicaid and exchange plans, so shifting to an exchange plan is less likely to cause a lapse in coverage or abandonment of prescription drugs or maintenance medications that control chronic conditions.

Medicaid expansion states

While much of the Medicaid news highlights significant decreases in enrollment, some states have recently expanded Medicaid eligibility or have programs in place to ensure their residents maintain insurance coverage.

One example is North Carolina, which launched its Medicaid expansion Dec. 1, 2023. Under the expansion, North Carolina now provides Medicaid for adults ages 19 to 64 even if they make too much money to qualify for traditional Medicaid but are below eligibility to receive subsidized private insurance. According to Clarivate data, the state’s Medicaid enrollment increased 10.6% to about 2.5 million between January 2023 and January 2024.

In April 2024, Mississippi lawmakers reached a tentative deal to expand Medicaid to include more than 200,000 additional low-income residents, although hurdles remain to finalize this expansion.

In March 2024, New York received approval for a five-year Medicaid expansion through April 1, 2028, extending eligibility to include individuals with incomes up to 250% of the federal poverty level (eligibility was previously capped at 200%).

New York and Minnesota are the only two states to provide the Basic Health Plan through a Section 1331 waiver since 2015. The program, called the Essential Plan in New York, was created under the Affordable Care Act as a health coverage program for low-income residents who are eligible to purchase coverage through the marketplace but whose income fluctuates above and below Medicaid and CHIP levels.

Texas, Massachusetts and Connecticut are among the numerous states approved for a Section 1115 waiver to ensure Medicaid coverage. The CoveredCT program, approved in December 2022, offers no-cost health and dental insurance to eligible residents between the ages of 19 and 64 who exceed the Medicaid income limit, but do not exceed 175 percent of FPL and are enrolled in Access Health CT, the state’s marketplace.

Key takeaways

Although growth in commercial and exchange enrollment will blunt some impacts, an increased uninsured rate will lead to increased uncompensated care, adding to cost pressures for health systems, especially safety-net hospitals that will see the highest volume of people cut from Medicaid. This may also lead to gaps in care, reduced drug adherence, increased emergency room visits and a decline in chronic care management.

With the latest surge in exchange enrollment, commercial payers that have avoided exchange marketplaces might have to reconsider that strategy as the exchange business has become entrenched as a critical component in coverage.

On the other hand, unprecedented exchange growth could be short-lived since the subsidy cliff that existed before the American Rescue Plan could return if the enhanced subsidies are not renewed in 2025. Depending on the results of the 2024 election, coverage and subsidies under the ACA may come under scrutiny again.

Learn more about Clarivate Managed Market Surveyor enrolled lives data and trends reports or get in touch with a Clarivate representative here.

This post was authored by: Bill Melville, Lead Healthcare Research and Data Analyst; Paula Wade, Lead Healthcare Research and Data Analyst; and Valerie E. Pillo, Senior Healthcare Research and Data Analyst.