Lives data updates and trends

Trusted insights with Managed Market Surveyor (MMS) & Pharmacy Benefit Evaluator (PBE)

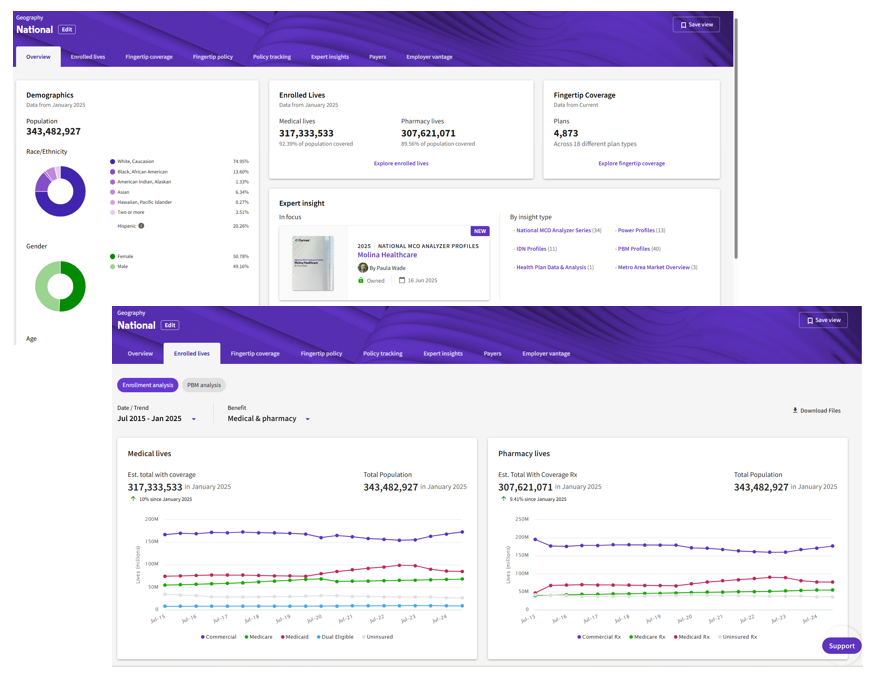

Build your market access strategy using accurate U.S. managed care enrollment data

Key 2026 highlights:

- Commercial: Fully insured enrollment declined 3.6% while self-insured increased 1.9% as of January 2026 compared to 6 months prior.

- Health Insurance Exchange (HIX): Enrollment declined 3.2%, which represented less than 1 million people despite the potential for a more precipitous decline.

- Medicaid: Medicaid enrollment declined 2.3% (nearly 2 million lives), including a 2.1% drop in managed care enrollment.

- Medicare: Medicare enrollment grew 3.0%, driven by fee-for-service gains as Medicare Advantage growth stalled amid policy headwinds.

Request more information

Lives data updates and trends

Health insurance exchange and Medicaid enrollment have both declined, showing the effect of government policies reducing the number of people covered by publicly funded insurance. As a result, access to care and prescription drugs are being impacted. At the same time, Medicare growth continues as baby boomers age into the program.

Pharmacy Benefit Evaluator (PBE)

& Managed Market Surveyor (MMS)

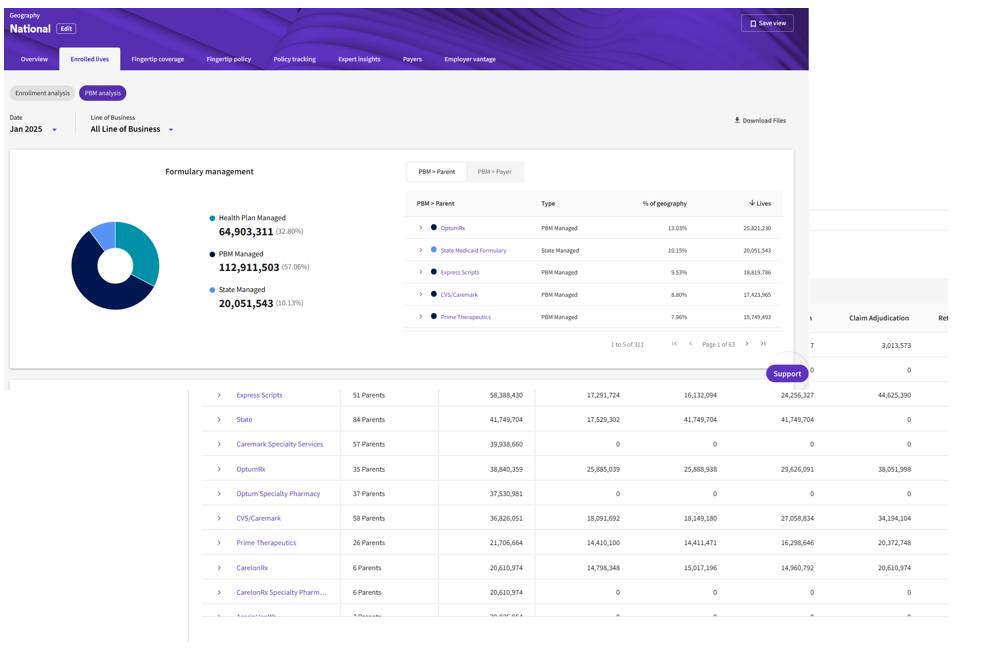

The Clarivate release of January 2026 PBE data in June will include the update of PBM GPO lives estimates. This new data will show the size and influence of GPOs negotiating prescription drug rebates, including the number of lives impacted at the GPO, PBM and payer (parent and subsidiary) levels for any geographic area in the U.S.

Here are the key highlights from the January 2026 data release:

Commercial coverage shifts toward self-insurance:

Overall commercial enrollment reported by health plans dropped by 0.6% as of January 2026 compared to six months prior. Fully insured enrollment – including health insurance exchange lives – was down 3.6%, while self-insured enrollment was up 1.9%.

Exchange enrollment declines less than expected:

Exchange enrollment was down 3.2%, which although significant, represented less than 1 million people losing coverage despite the specter of a potentially more precipitous decline.

Medicaid enrollment continues to decline:

Medicaid enrollment dropped by nearly 2 million, which is a 2.3% decline, including a 2.1% reduction for managed care plans.

Medicare growth shifts back to fee-for-service:

Medicare enrollment increased by 3.0% with growth concentrated in fee-for-service coverage as Medicare Advantage enrollment stalls amid less favorable government policies for managed care plans in this sector.

Here is additional background on market dynamics impacting enrollment:

Many regional health plans across the country are facing mounting financial pressure as healthcare costs continue to rise and competition within the market intensifies. These challenges have made it difficult for smaller regional payers to maintain sustainable margins, resulting in several regional payers scaling back operations, exiting certain markets, or closing entirely. For example, Health Alliance Medical Plan ceased all operations as of January 1, 2026. Larger payers have been able to remain stable in the commercial medical market or have even grown by focusing on self-insured products.

January 1, 2026, marked the expiration of marketplace enhanced subsidies and changes in eligibility criteria for premium tax credits. In response, some states have offered their own state-funded subsidies to help reduce the cost of premiums to qualified consumers. Aetna has completely left the marketplace, dropping coverage in 17 states as of 2026. Other payers have followed suit by exiting the market altogether, leaving a service area, or reducing their overall membership. Centene reduced its exchange marketplace enrollment by more than 2.2 million lives.

Insurers are responding to changes in medical trends and decreasing federal funding by re-evaluating their place in the Medicare Advantage (MA) market. While payers like UnitedHealthcare are pulling back their offerings and reducing MA enrollment as of January 2026, others like Humana have increased their membership in the Medicare Advantage space.

The 2026 Medicaid landscape reflects a market that is stabilizing following almost six years of unprecedented operational and eligibility related disruption. While broad national trends suggest moderation in overall enrollment movement, the underlying drivers remain highly state-specific and continue to vary significantly across medical and pharmacy lines of business. California and New York have the highest share of their populations enrolled. States differ widely as some face funding gaps or new work requirements. The takeaway is that each state’s situation is unique. Managed care procurement activity, state policy changes, fee-for-service transitions, pharmacy carve-out structures, and Medicaid adjacent coverage programs (such as the Basic Health Program) are all contributing to evolving enrollment dynamics. As a result, market shifts in 2026 are indicators of broader structural and operational transformation occurring across the Medicaid ecosystem.

Each data purchase comes with the support and insights of our subject matter experts

- Our analyst team goes above and beyond to identify key trends and insights from the latest data. With a deep understanding of the market, they provide analysis with insights you can rely on.

- We want you to get the most out of your purchase. That’s why we provide complimentary training sessions to help you understand the data and its applications. Our subject matter experts will be available to guide you through the insights and help you make informed decisions.

How our enrollment and PBM data informs customer strategies and decision making

- Inform your payer contracting strategy. With accurate and up-to-date information on payer market share, you can make strategic decisions to optimize your market access.

- Stay ahead of the competition. Analyze the shifts and trends in enrollment to identify opportunities and grow the accessibility of your therapies or maintain your market position.

- Navigate benefit design using influence. Understand the influencers of benefit design for key accounts and markets and navigate benefit design strategies more effectively.

Don’t miss out on the opportunity to equip yourself with essential enrollment data and insights. Complete the form to start leveraging the power of MMS Enrolled Lives data and trends reports to drive your market access strategy forward. Also consider purchasing Pharmacy Benefit Evaluator (PBE), which complements MMS and provides pharmacy benefit manager to health plan affiliations data with details on relationship and contract design showing control of formulary decision making and access.

The MMS Enrolled Lives data release occurs twice each year—January data point released in June followed by the July data point released in December. Stay tuned for future updates.

Complete the form below to learn more about our offering and make a purchase: